*updated 12-5-2025

For Texas property owners exploring alternatives to traditional real estate transactions, owner financing offers a direct and flexible method of sale. This guide explains how seller-financed agreements work, purchase price agreements including key legal considerations and steps involved in structuring the deal.

How to Sell Your House with Owner Financing in Texas

Selling a house the traditional way? Or thinking about seller financing in Texas to sell your house fast?

The bureaucratic loan process doesn’t always cut it anymore – especially if your ideal buyer is getting turned down by banks left and right.

That’s where owner financing, often called “seller financing,” comes in. It’s creative way to sell that puts you, the homeowner, in control.

In Texas, it’s not just legal… it’s surprisingly common.

So, how does owner financing in Texas work?

You’re basically stepping into the lender’s shoes. You get to be the bank!

Instead of your home buyer going through a mortgage company, they’ll make monthly payments directly to you.

You set the terms, you manage the deal… and yes, that includes the interest rate, payment schedule, and even a balloon payment if it fits.

No traditional loan. No waiting on underwriters. No bank hoops to jump through.

This type of Texas property sale, officially known as an owner financing arrangement gives you full control over how the deal is structured. And in a real estate market like Texas, where homebuyers may not qualify for traditional lending product, the deals that are creative and flexible can be a serious edge.

Let’s say you’re selling to a first-time homebuyer. Or maybe a family member. Or someone rebuilding their credit after a rough patch.

Owner financing opens the door for those buyers, and gives you the chance to sell faster, with more control over the process and payment terms.

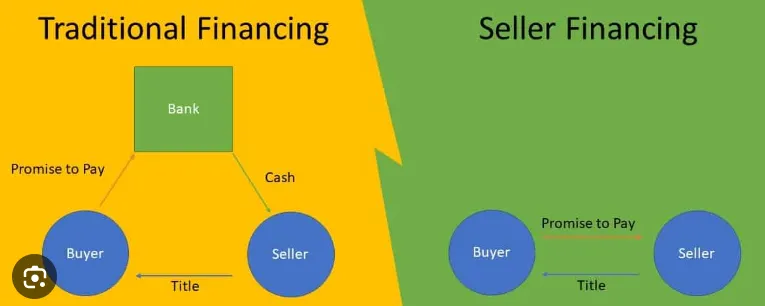

What is Owner Financing and How Does It Work?

But let’s pause for a sec… what exactly is owner financing, legally speaking?

It’s a seller financing transaction where two core documents come into play:

- A promissory note, which lays out the loan amount, interest rate, monthly payments, and any balloon payment down the road.

- A deed of trust, which acts as a lien and protects you if the buyer defaults.

In some cases, especially with an existing mortgage still on the property, sellers might use a wraparound mortgage — basically wrapping the new loan around the old one.

The buyer pays you, you pay your lender, and everything moves forward.

It’s not one-size-fits-all.

That’s the beauty of seller financing.

You can tailor the agreement to fit your buyer, your property, and your goals — whether that’s generating monthly income, getting a higher sale price, or closing the deal fast.

When And Why Owner Financing in Texas Is a Smart Move for Home Sellers

Flexible terms attract more buyers

If you’ve got a house to sell and you’re not getting bites from buyers with bank pre-approvals, don’t take it personally.

Take control.

Owner financing in Texas opens the door to a whole new group of homebuyers who’ve been shut out by traditional lenders.

We’re talking first-time homebuyers. Business owners. People with thin credit check files. Even folks recovering from financial setbacks and poor credit.

With seller finance, these buyers finally get a shot at homeownership and you get a bigger pool of serious offers.

More potential buyers means more demand.

That alone can help you sell faster and for a better price.

Monthly payments create steady cash flow

And here’s the kicker: you don’t have to sacrifice returns.

When you offer monthly payments instead of a lump sum, you create a steady, predictable income stream during the repayment schedule.

Think of it like becoming your own mortgage company… except with better terms for you.

Many sellers set a high interest rate as compared to a traditional mortgage lending, which means more cash in your pocket over time.

You may also be able to ask for a higher sale price.

Why?

Because buyers are often willing to pay more in exchange for flexible repayment terms. You’re offering something banks can’t.

That’s worth a premium.

You control the property sale — not the bank

Owner financing arrangements often close faster than conventional deals.

No bank delays. No underwriting limbo.

Just a direct agreement between you and the buyer. In hot Texas markets like Dallas, Fort Worth, or San Antonio, that agility can give you a serious edge.

Why Buyers in Dallas and Arlington Love This Homeowner Option

Homeownership without a bank loan

Now flip the script.

If you’re the buyer in Dallas or Arlington, chances are you’re already bumping into roadblocks.

High home prices, tight lending, long approval timelines.

Owner financing solves all of that.

For buyers with credit issues, self-employment income, or unique life situations like buying from a family member, this path is often their best shot at landing a home. They get a chance to build equity in real property without the stress of creditworthiness and qualifying for a conventional loan.

Ideal for first-time buyers and family sales

It’s especially helpful in situations where a buyer and seller already know each other.

Say, a family member helping out another family member.

You don’t have to involve a mortgage company to get the deal done. That cuts down on paperwork, delays, and fees.

A win-win deal structure for both sides

For the seller, this means you get a real buyer who’s motivated and ready.

For the buyer, it’s a chance to get into a home they might otherwise not qualify for.

It’s the kind of win-win that makes owner-financing transactions such a powerful tool in the Texas real estate market.

Steps to Sell Your Texas Property with Owner Financing

Prepare your home and legal documents

Before you can offer owner financing in Texas, you’ve got to get your house, and your paperwork, in order.

Start with the basics. Make sure the home is clean, presentable, and move-in ready, especially if you’re trying to attract serious buyers.

Now let’s talk legal prep.

Selling a home this way isn’t as simple as shaking hands and collecting checks.

You’ll need the right legal documents in place.

That means checking your property title to make sure there are no liens or disputes, then working with a title company to secure title insurance. This protects both you and the buyer, making sure the sale of your real property is legit and risk-free.

Next, you’ll want a solid purchase agreement that lays out the terms: the sales price, the down payment, who’s paying the property taxes, and what happens if either party backs out.

This isn’t something to DIY.

Bringing in a real estate lawyer is smart.

They’ll make sure everything aligns with the Texas Property Code and state laws, especially if the property has an existing mortgage or unusual ownership history.

Set up the owner financing agreement

Once the sale terms are squared away, it’s time to build the actual financing arrangement. This is where you shift from seller to lender.

The heart of this deal is the owner financing agreement, which includes two key documents:

- The promissory note, which outlines the loan amount, interest rate, payment schedule, and terms of repayment.

- The deed of trust, which acts as a lien and gives you recourse if the buyer stops paying.

Want to include a balloon payment? Need a due-on-sale clause to protect your interests if the property is resold? Spell it out here. Every detail matters.

To stay on the right side of the law, consider hiring a mortgage loan originator or having your attorney structure the deal.

Depending on how many seller-financing deals you do, federal laws like the SAFE Act or Dodd-Frank Act may require it.

You’ll also need an amortization schedule so everyone knows how payments break down over time.

This helps your buyer understand where their money is going, and helps you stay organized as payments come in.

Finally, don’t overlook the closing process. Just because there’s no bank doesn’t mean there’s no paperwork. A professional closing ensures the owner financing transaction is properly recorded, and that you’re legally protected from day one.

Challenges in Owner Financing Transactions

Risks and how to protect yourself

Owner financing can open a lot of doors, but it’s not without risks.

One of the biggest?

When a homeowner stops making mortgage payments.

If a buyer defaults, you could be stuck dealing with a legal mess that eats up time, money, and patience.

That’s why your first line of defense is your paperwork. Make sure your owner financing agreement spells out exactly what happens if a payment is missed. Late fees, grace periods, foreclosure rights — get it all in writing.

You’ll also want to screen your buyer.

Just because you’re not a traditional mortgage lender doesn’t mean you should skip the background check.

Pull a credit score report, ask about income, and get a real sense of their financial habits.

If something feels off, it probably is.

There are also tax implications to consider.

Since you’re collecting payments over time instead of getting the full sales price up front, your income will be taxed differently.

A good real estate accountant can walk you through how to report the income and handle the property taxes. In some deals, you may even need to keep paying the property taxes yourself, depending on the structure.

If you’re using a wraparound mortgage or land contract, you’ll need extra legal protections to make sure your own obligations, like paying an existing mortgage, are still covered.

This is where working with a real estate lawyer really pays off.

Legal requirements and licensing considerations

Just because this is a private deal doesn’t mean you’re off the legal hook.

Seller financing transactions are subject to both state and federal laws.

In Texas, the Texas property code outlines your responsibilities.

Here’s the short version.

If you’re offering owner financing more than once or twice, you may need to meet certain licensing requirements, or hire a licensed mortgage loan originator to structure the deal on your behalf. This protects the buyer from predatory lending, and it protects you from lawsuits.

A real estate lawyer can help you stay compliant.

So can working with a title company that understands seller financing transactions. They’ll walk you through the closing process, file the right paperwork, and make sure your rights as the seller are fully protected.

Bottom line?

The more you treat this like a real business deal, the safer you’ll be.

Real-Life Examples and Insights from Texas

Owner financing success in Dallas, Fort Worth, and San Antonio

In Texas cities where the housing market is tough and prices keep rising, seller financing deals are helping homeowners and investors get creative.

We’ve seen it firsthand. In Dallas and Fort Worth, more and more sellers are skipping the traditional route and offering flexible financing terms to close faster and reach more potential buyers.

Take one real estate investor in Dallas TX. He had an older investment property that needed work. Listing it the usual way would have meant lowball offers or sitting on the market too long.

Instead, he created an owner financing agreement that appealed to a homebuyer who didn’t qualify for a conventional loan but was ready to take on the repairs (he was a handyman on the weekends). The seller locked in a strong sales price and regular payments.

The buyer got equity and a path to ownership.

That’s the kind of deal where everyone walks away with something they need… whether it’s time, cash flow, or a foothold in the Dallas real estate market.

When to use seller finance for investment property

The owner financing option isn’t just for people selling their primary residence.

It’s also a powerful tool for moving investment property or structuring deals with long-term upside.

One popular approach is lease-purchase agreements. These work especially well in commercial real estate, where the buyer might not want to lock in a purchase right away, but still wants control of the space and a timeline to buy.

If the seller and buyer already have a relationship (maybe it’s a family member or business contact), seller finance process can be a good idea to cut through red tape and find an easier way.

No waiting on underwriters or dealing with banks that don’t understand the unique nature of the deal.

You also get to shape the terms around your desired profit and timeline. Want to keep some income flowing in before handing over the keys? Structure it that way. Want to wrap it up with a balloon payment down the line? Build it into the real estate contract.

Seller Financing in Texas: Common Questions Answered

Is Owner Financing Legal in Texas?

Yes, owner financing is legal in Texas under the Texas Property Code and federal regulations. Sellers can provide financing directly to buyers instead of using a bank. It’s important to follow proper contracts and disclosures to protect both parties during the transaction

How Does Seller Financing For A House Work in Texas?

Seller financing in Texas allows the homeowner to act as the lender. The homebuyer makes payments directly to the seller under a promissory note and deed of trust. This home sale option bypasses banks and helps buyers with limited credit history qualify for homeownership.

Who Holds The Deed on a House With Seller Financing in Texas?

In Texas, the home buyer typically holds the deed while the seller retains a lien until the loan balance is paid off. This framework protects the seller if the buyer defaults on payments and ensures the buyer has ownership rights while making scheduled payments.

Are There Closing Costs With Seller Financing?

Yes, seller financing usually involves closing costs, though they are often lower than traditional bank loans. Typical expenses include title work, recording fees, and legal documentation. Because the process is streamlined, sellers and buyers often save compared to conventional mortgage closings.

What Are The Risks of Seller Financing in Texas?

Risks include buyer default, enforcement challenges, and managing tax or lien responsibilities. With proper contracts and professional guidance, many home sellers reduce these risks. In Texas, trusted home-buying companies like Bright Bid Homes provide support to structure secure, legally sound seller financing agreements

What is the TREC Seller Financing Addendum?

The TREC seller financing addendum is a Texas Real Estate Commission form that outlines loan terms, interest, payment schedule, and homebuyer obligations. It protects both parties by ensuring the financing agreement is clearly documented, legally compliant, and enforceable in Texas real estate transactions..

Key Takeaways For Selling Your Texas House With Owner Financing

When seller financing works, it works for everyone.

It gives you, the seller, control over the terms, the timeline, and the income stream.

It helps buyers who don’t fit into a bank’s box find a real path to Texas homeownership. And it can sell your property faster without sacrificing value.

But the key is doing it right.

You’ll want more than a handshake and a homemade contract.

A real estate lawyer can help draft terms that protect your interests. A title company will make sure everything’s recorded correctly. And if you’re feeling unsure about where to start or how to structure the deal, you’re not alone.

That’s where we come in.

At Bright Bid Homes, we’ve helped countless Texas homeowners sell their properties through smart, customized seller financing strategies.

Whether you’re offloading an investment property or working a unique buyer situation, we can walk you through the process, answer your questions, and even step in as a buyer ourselves.

Owner financing isn’t a one-size-fits-all solution. But with the right guidance, it can open up real options, real returns, and real peace of mind.

If you’re considering this type of sale, let’s talk. Bright Bid Homes is Texas-based, family-run, and here to help you get the deal done the right way.

Contact Us

Want To Learn More? Let’s Start A Conversation! Please Fill Out This Quick Form And We’ll Get Back To You Right Away.

** Disclaimer: This article is for informational purposes only and does not constitute legal advice, financial advice, or a substitute for consulting a licensed agent or real estate attorney. Every owner finance transaction involves unique circumstances, including legal title issues, financial institution guidelines, and the buyer’s ability to qualify for conventional financing options or mortgage alternatives. Seller finance arrangements in Texas should be reviewed with a qualified professional to avoid legal issues related to the deed of trust, land trusts, licensing, buyer disclosures, and other real estate law issues.

While owner financing can offer faster closing timelines and expand your buyer pool, it’s important to weigh the pros and cons of owner financing against traditional real estate deals. Always consult a real estate lawyer before finalizing any selling process involving non-traditional types of financing.

*** About the Authors: With over 20 years of experience in real estate and 2,900 transactions completed, Hilary and Patrick Schultz bring practical insight to Texas homeowners exploring options like owner financing. Hilary is a licensed Texas Realtor and a recognized Zillow Top Agent. Through their family-operated company, Bright Bid Homes, they specialize in working with sellers who need flexible, ethical solutions for complex property situations. Hilary also gives back to her community by serving on the executive board of her local Texas PTA. To explore their background, visit their About our Texas company, check client online reviews, view Hilary’s Zillow badge, or verify her TREC license.